You've saved up 20% for a down payment. The conventional wisdom says buy a house. But what if you rented instead and invested that money? The answer might surprise you—and it definitely changes over time.

The Conventional Wisdom

Everyone tells you to buy. Build equity. Stop throwing money away on rent. Real estate always goes up. You've heard it a thousand times.

But when you actually run the numbers over 30 years with realistic assumptions for rent inflation, home appreciation, and investment returns, something interesting happens. The answer isn't as straightforward as the real estate industrial complex wants you to believe.

The Two Scenarios

Let's compare two paths using realistic assumptions based on historical data:

🏠 Buying a Home

Put 20% down, pay mortgage, taxes, and maintenance. Build equity as the home appreciates over time.

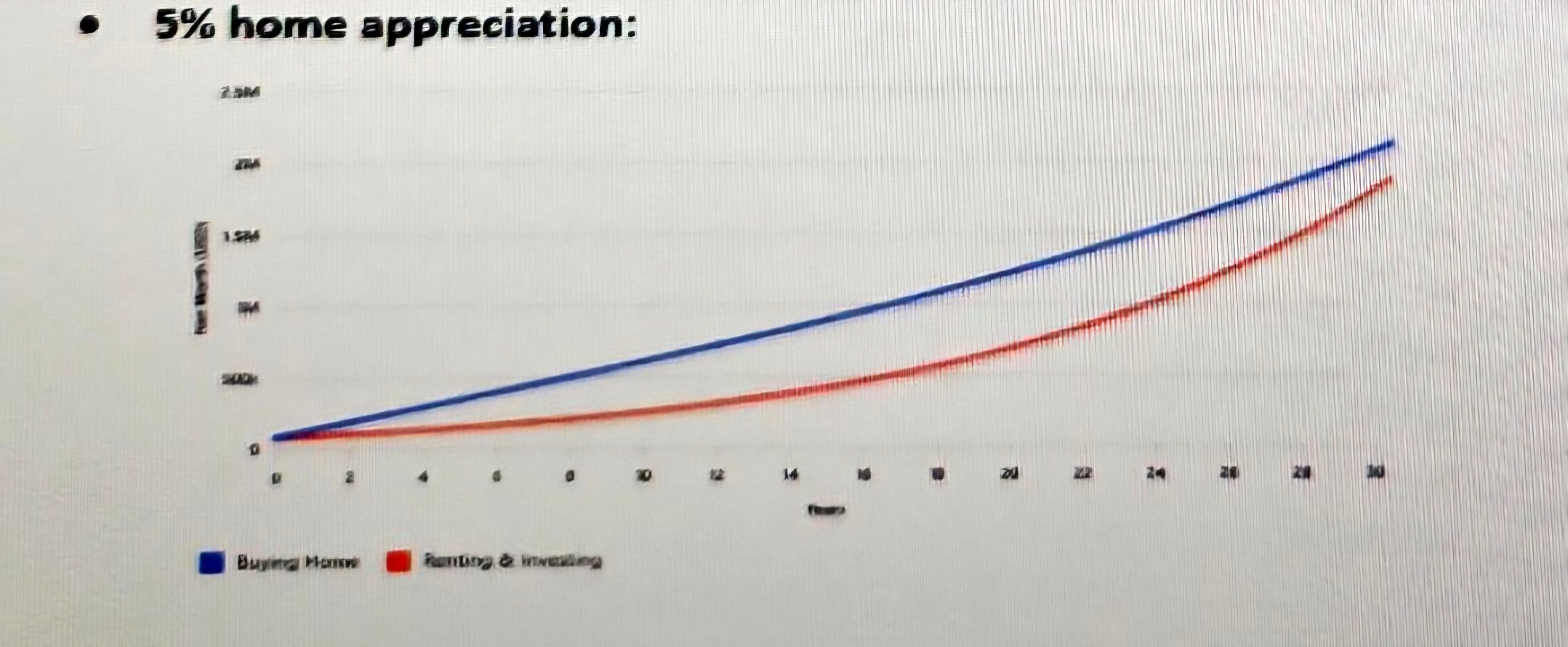

Appreciation: 5% annually (historical average)

📈 Renting & Investing

Keep renting, invest the down payment and the difference between rent and ownership costs.

Investment return: 10% annually (historical stock market average)

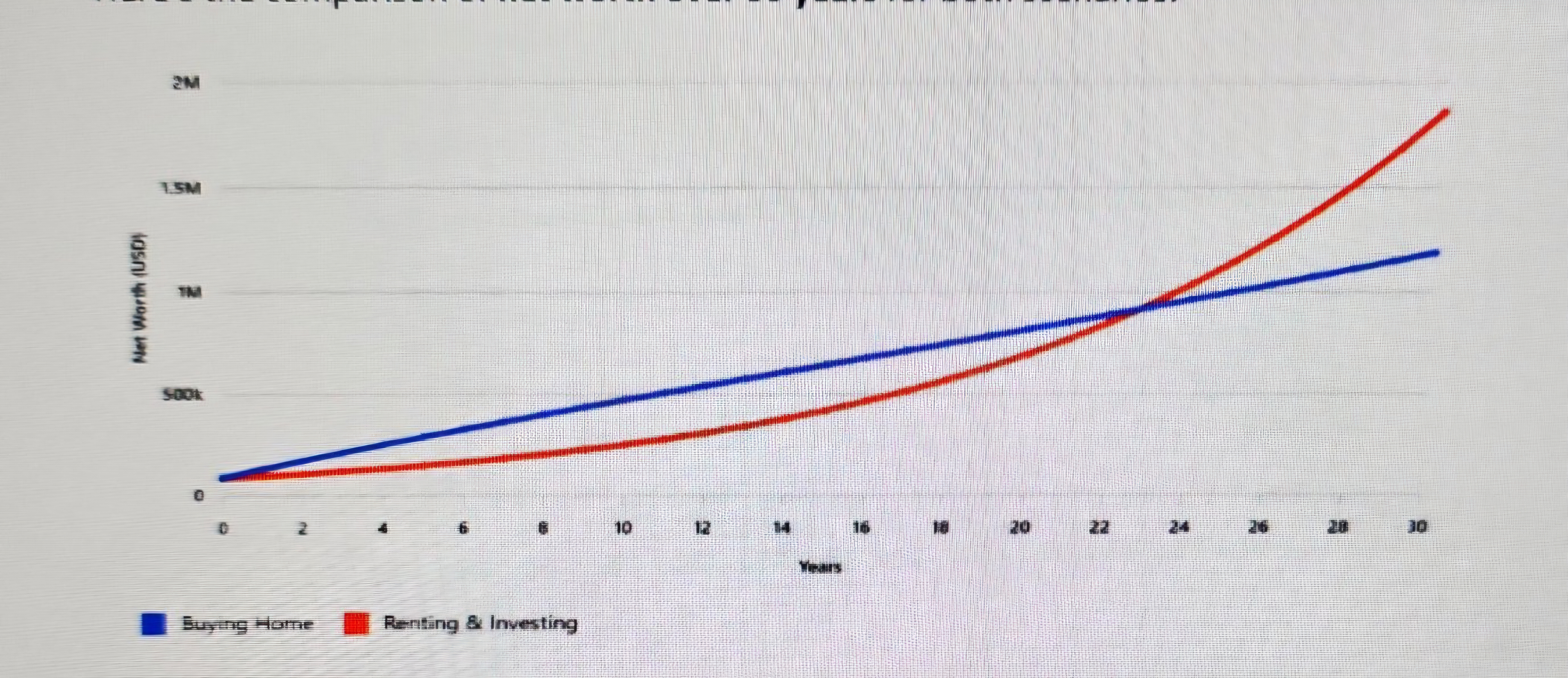

The Surprising Results

Over 30 years, see the two scenarios with 3% CAP vs 5% CAP end up in similar territory—butf they get there very differently.

Why Renting Wins Early

In the first 15-18 years, renting and investing dominates if CAP returns are lower at 3%. Here's why:

When you buy a home, your down payment goes into an illiquid asset appreciating at 3% annually. Meanwhile, you're paying mortgage interest, property taxes, insurance, and maintenance—costs that renters avoid. That difference gets invested and compounds at 10% annually.

The investment account grows faster because it's purely growth without the drag of ownership costs. Meanwhile, your home equity builds slowly in the early years because most of your mortgage payment goes to interest, not principal.

Why Buying Catches Up

Around year 18-20, the math shifts but if the CAP rate is 5% the home almost immediately has more value. Your mortgage payment stays fixed (if you have a fixed-rate loan) while rent keeps increasing with inflation. That difference narrows, reducing how much extra you can invest.

Simultaneously, more of your mortgage payment shifts from interest to principal, accelerating equity buildup. The home's appreciated value compounds on a larger base. By year 20, the trajectories cross even with 3% CAP rate on the house..

The Critical Assumptions

These results depend heavily on your assumptions. Change any of these variables, and the outcome changes dramatically:

Home appreciation: The model assumes 5% annually. If your market only appreciates at 3%, renting and investing wins by a landslide. If it appreciates at 7%, buying dominates from day one.

Investment returns: Assumed at 10% annually (historical S&P 500 average). A bear market in your early investing years can crush this advantage. Consistent returns matter.

Rent inflation: The model assumes rents increase steadily. If you live in a rent-controlled area or a market with stagnant rents, renting and investing stays ahead longer.

Discipline: This only works if you actually invest the difference. If you rent cheaply but spend the savings, buying wins every time.

What This Actually Means

If you're planning to stay put for 30+ years, buying probably wins—assuming you're in a market with normal appreciation rates. But if you're mobile, career-focused, or uncertain about long-term plans, and live in an area with low housing CAP rates, like 3%, the first 18 years favor renting and investing.

The dirty secret is that most people don't stay in one home for 30 years. The average American moves every 5-7 years. If that's you, buying and selling repeatedly with transaction costs, realtor fees, and market timing risk might mean you never actually capture the long-term advantage of ownership.

The Intangibles

Numbers don't capture everything. Homeownership provides stability, control, and psychological benefits that aren't in any spreadsheet. Renting provides flexibility, lower risk, and freedom that numbers also can't measure.

The point isn't that one path is definitively better. It's that the conventional wisdom—"always buy"—is mathematically wrong for many situations and time horizons.

Run your own numbers with your local real estate prices, expected rent, and realistic assumptions about how long you'll actually stay. The answer might not be what everyone's been telling you.